The Business of Africa Data Centres.

Africa Data Centres are becoming an alternative asset class as the continent’s digital infrastructure ecosystem which includes fibre-optic broadband expansion and telecom towers grows due to increased mobile data consumption, a vibrant tech sector, high cloud computing and social media usage.

Why it matters: According to a report by global real estate investment firm CBRE Investment Management, “Core infrastructure is guided by a private market perspective that identifies core infrastructure as the marriage of a physical asset providing society with an essential service with resilient long-term cash flows” which the Africa Data Centre Industry offers.

The players: There are currently 10 players dominating the markets namely: Africa Data Centres, MainOne., BCX, Medallion Data Centres, IX Africa, Open Access Data Center, PAIX, Paratus and 21st Century Technologies who have actively been raising funding for their expansion plans.

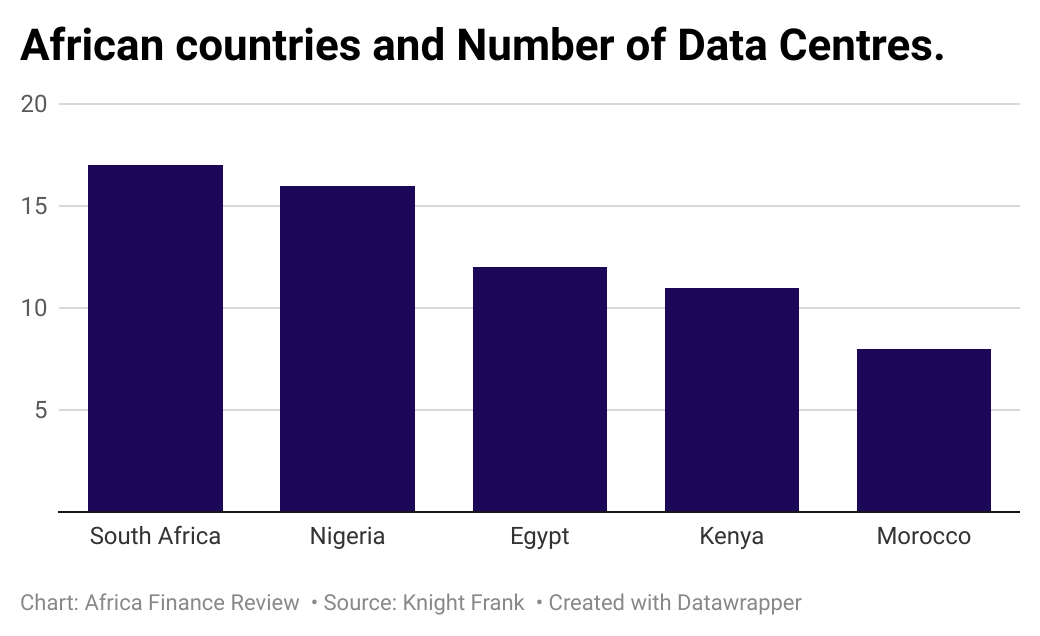

And the numbers: The African warehouse-type of real estate market with physical space, security and cooling services for multiple chargeable tenants is expected to compound annually at a growth rate (CAGR) of approximately 15% from 2020 to 2026 and grow to US$3bn by 2025. The rapid growth of data centres across Africa according to the KnightFrank -Africa Report 2022, reflects the demand across the continent.

Africa is experiencing the fastest increase in internet penetration worldwide with data consumption expected to increase by 45% each year until 2025. Even with its high barrier to entry and need for local knowledge, sustainability-linked debt facility and significant investments offer predictable growth with consistent cashflow if targeted at creditworthy customers with lengthy contracts such as local banks and Telcos.